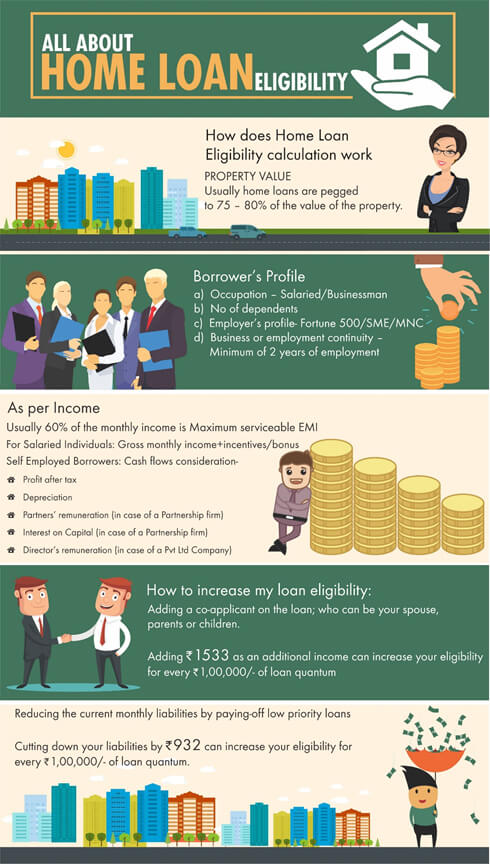

How Does Eligibility Calculation Work?

Loan Eligibility is a factor of the following criteria:

Property Value – Usually home loans are pegged to 75 – 80% of the value of the property, as determined by the lender.

Borrower’s Profile – The key aspects that come into play are:

As per Income – Usually banks cap the Maximum serviceable EMI of a prospective Home loan to 50 – 60% of the Gross Monthly income. In case of self-employed borrowers, the banks look at the cash flows generated from the business such as:

How to increase my loan eligibility:

Adding a co-applicant on the loan; who can be your spouse, parents or children.

For every Rs.1,00,000/- of loan quantum at a 20-year tenure & 9.50% Interest rate, it takes about Rs.1533/- of additional income.

Reducing the current monthly liabilities by paying-off low priority loans

Here’s a simple calculator that shows what happens to your home loan eligibility if you cut out an existing EMIs of any other loan type

Only way we can serve you is hear from you. Provide us with your contact information and our loan experts will help you at every step.